Working Draft: Beer Market Structure

Capture, Concentration, and Anti-Trust

This article is the second instalment in my Working Draft series, discussing the economics of craft beer. For more background on the brewing industry and relevant definitions you can read my introduction here.

In November 2025 Lina Khan, now serving on the transition team for New York’s incoming mayor Zohran Mamdani, flagged the pricing of beer at large public venues as an example of what might be termed an “unconscionable” business practice (NYC Admin. Code §20-700)1. Despite falling not far from the league average, the high price of concessions at New York’s Yankee Stadium is a constant source of indignation among stadium goers, and a natural issue for the former FTC Chair. A stadium concession price cap is, in some sense, an example of antitrust intervention, albeit in a very narrow monopoly market. Whatever New York City ultimately does with its longstanding “unconscionability” consumer-protection rule typically applied to rent-gouging and crisis pricing, the legal intervention would apply only to a handful of high-traffic venues and would not have much effect the broader functioning of the local beer market. So why all the attention?

Khan’s comment captured national attention precisely because stadium beer marks a unique case of a good priced at the far reaches of consumers’ willingness to pay. What may in theory might be “efficient” pricing, doesn’t always feel that way. A $15 beer (the cost at Nationals Park, Yankee Stadium falls closer to the $8 mark) at a baseball game should be no surprise, but nevertheless painful for the consumer. Stadiums epitomize natural monopoly. Fans cannot exit to find price-competitive options for beer without forfeiting the very reason they are present. Vendors typically operate under exclusive multi-year contracts, often granted to a single food and service provider, which effectively eliminate the possibility of price discipline from market competition. Exclusive venue contracts are standard in U.S. sports, with concessionaires such as Aramark, Delaware North, or Legends operating under multi-year agreements that typically include sizable upfront fees and exclusivity rights. Even where multiple beer brands appear on offer, the supply chain behind those brands tends to be coordinated by a single concessionaire with exclusive control over purchasing, distribution, and retail point-of-sale inside the venue. In economic terms, the stadium is a self-contained economy with limited actors, insulated from the market pressures that operate outside its walls.

The logic of captive-market pricing might give us some insight on the role of market capture and antitrust in beer and brewing more broadly. Stadium concessions expose a deeper, structural logic that appears throughout the history of brewing in the United States: where competition is constrained, prices adjust, and consumer choice narrows. This dynamic, while seemingly unique to events held at ticketed venues, offers something like a natural experiment in market concentration: a space where the usual point-of-service competitive mechanisms are intentionally suspended. Understanding how competition functions, or does not function, in this environment provides a clear view of how structure matters for relevant economic outcomes, and how pricing can under some conditions be less about cost and more about market structure and the regulatory environment. The stadium case therefore offers a conceptual point of departure for assessing market capture in brewing more generally, from national concentration to state distribution bottlenecks, and venue level consolidation and capture.

The National Market and Brewery Concentration

Looking at the beer industry from roughly 1950 to 2000, one of the largest contributors to increasing concentration was a rising minimum efficient scale for brewing, limiting the maximum feasible number of firms to around five national producers.2 What had once been a landscape of geographically distinct regional breweries, hundreds operating with local distribution footprints, gave way to an era dominated by a handful of mass-producers. Ironically, this meant that the overall variety in the domestic market looked a lot like the five or so beers that might be listed on a stadium concession board. However, the reasons for this shift were legal and economic rather than cultural or taste-based, though cultural changes would certainly follow.

In 1950, the structure of the U.S. beer market still reflected the older regional model that had persisted since Prohibition. The largest breweries by national market share were Schlitz at 6.8%, Anheuser-Busch at 6.5%, Ballantine at 4.8%, Pabst at 4.7%, and Miller at 3.2%.3 Even the so-called “big” brewers were, in practical terms, still modest regional firms. No single company held more than seven percent of the national market, and dozens of mid-sized brewers remained competitive within their own distribution territories. Coors was at that point was relegated to the smaller Western market and did not distribute nationally, and would not enter true national competition until the late 1960s and 1970s. The market of 1950 was thus dispersed, locally oriented, and only regionally consolidated.

This would change with the introduction of greater competition and economies of scale. Large-scale lager brewing required substantial investment in stainless-steel fermentation vessels, refrigeration systems, bottling and canning lines, large, dedicated warehouses, and a national distribution network. Firms able to deploy these investments could spread fixed costs across tens of millions of barrels, driving down average costs to levels that small and mid-sized brewers simply could not match. And so began the race to the bottom, as firms competed on cost efficiency rather than product differentiation or variety.

By the late 1970s the regional brewer had all but disappeared. The combination of large-scale advertising, advances in refrigeration and transport, the adoption of highly efficient continuous-flow brewing systems, and a series of targeted acquisitions by the emerging national players transformed the competitive landscape.4 By 1977 Anheuser-Busch’s national market share had jumped to 23.3%, Miller to 15.4%, Schlitz to 14.1%, Pabst to 10.2%, and Coors to 8.17%. What had been a field of dozens of regionals was now a tightly concentrated national market dominated by five firms. Anheuser-Busch, still only a medium-sized player in 1950, had become the country’s first true brewing giant, controlling nearly a quarter of all domestic beer sales. Miller’s rapid ascent, fueled by the success of Miller Lite after 1975 and significant marketing investment, pushed it past Schlitz, which was beginning to falter after production-quality problems and strategic missteps. Coors’ move into broader distribution brought it into the top tier almost immediately.

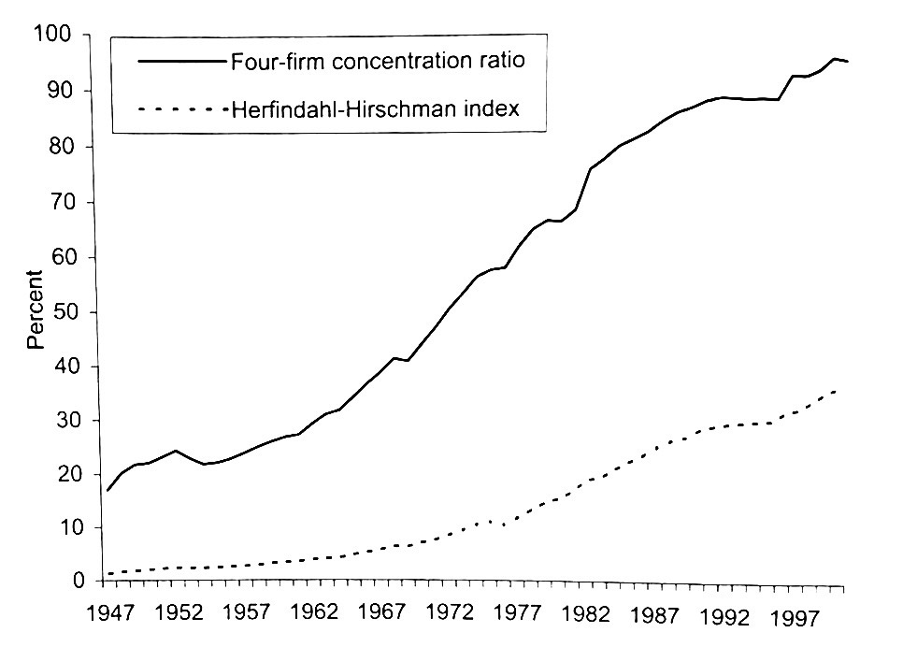

By the end of the decade, the U.S. beer industry had crossed a structural threshold: the top five firms accounted for more than 70 percent of national sales, and the four-firm concentration ratio, a traditional measure of market consolidation, had climbed above levels that economists typically associate with oligopolistic behavior. The shift between 1950 and 1977 was not gradual or incidental. It was a decisive reorganization of the American beer market around economies of scale, national advertising budgets, and emerging nationwide distribution systems. The resulting concentration would define the industry for the next generation.

Figure 1: Brewery Concentration 1947-2000

Figure 1: Beer market concentration from post-prohibition low to peak in 2000. via Tremblay, Victor, and Carol T. Tremblay. The U.S. Brewing Industry: Data and Economic Analysis. MIT Press. Appendix A.

Economists Martin Stack and Victor and Carol Tremblay respectively describe the period from the 1950s through the 1980s as one of relentless consolidation. Major firms absorbed competitors, expanded their marketing budgets to previously unimaginable levels, and developed highly standardized products designed to minimize variation. Uniformity served a purpose. American adjunct lagers had long fermentation and conditioning times, and the consistent production methods favored companies with scale. It was not that consumers overwhelmingly preferred these beers at first (in fact they have always been a source of complaint); instead, these beers became the center of the market because they were the least offensive products that could be produced, advertised, and distributed at scale.

By the 1980s, the United States had effectively become a national market for beer and limited regional differentiation, with the top three firms controlling more than 70 percent of total sales. By 2000, that figure approached 80 percent or more than 93 percent if we expand the scope to the top ten. Despite the appearance of choice on market shelves, rows of identical, pale lagers distinguished primarily by label design, the product diversity of American beer was at a historic low. The national market came to resemble the closed environment of the stadium: a small number of producers, a limited set of available offerings, but prices nationally showed a fierce race to the bottom even amidst high market concentration.

Antitrust enforcement in the American beer industry has always reflected larger shifts in how regulators understand competition. Around the mid-century the dominant concern was horizontal consolidation among the major national brewers, a trend driven by rising minimum efficient scale and the collapse of the old regional system. Early on, the Department of Justice challenged a handful of mergers under Section 7 of the Clayton Act, most notably United States v. Pabst Brewing Co. (1966), where the Supreme Court held that even relatively small acquisitions could violate antitrust law when they occurred in already concentrated markets.5 Around the same time, FTC v. Procter & Gamble Co. (1967) and other decisions broadened the analytical focus from price effects to structural harms. These rulings reflected mid-century suspicion toward conglomerate and horizontal mergers, and for a brief period stemmed the tide of consolidation in brewing. But by the late 1970s and early 1980s, with the emphasis on consumer price as the metric of competition, antitrust enforcement of major brewers softened, paving the way for mega-mergers to come.

The DOJ’s 1982 Merger Guidelines formalized this more permissive approach. As long as the major brewers could argue that large-scale production delivered lower consumer prices, and would regulators allow consolidation to continue. The result was a national market in which Anheuser-Busch, Miller, and Coors accounted for the vast majority of sales by the end of the century. But this would begin change as even in the late 90s the number of breweries nationwide had started to rise again as the early craft brewers meaningfully entered the market.

How Craft Brewing Overcame the Scale Barrier

Given this history, the explosion of small breweries beginning in the late 1990s and accelerating through the 2000s is something of an economic puzzle. Today there are nearly 10,000 breweries operating in the United States, and beer imports are higher than ever, without a dramatic increase in total consumption. Per-capita beer consumption has been relatively flat since the mid-1990s, yet breweries have multiplied at a rate that would have been inconceivable during the era of industrial consolidation.

Signed into law by President Carter in October 1978, HR 1337 legalized the practice of homebrewing at the federal level, playing a crucial role in the development of the modern American craft beer movement. Prior to this legislation, homebrewing was expressly prohibited by federal law under the Alcohol Beverage Control Act of 1933. The 1978 amendment removed the last federal barrier, allowing individuals to produce small quantities of beer for personal use without a license. It did not immediately create a craft industry, but it opened the door to a culture of innovation that would become its foundation.

Homebrewing has always encouraged innovation and experimentation; new recipes, yeast strains, hopping techniques, equipment improvements, and the deregulation of the practice allowed that experimentation to flourish in public. Once the federal prohibition was lifted, homebrewers could collaborate openly, share knowledge, and refine techniques. Clubs and associations formed, competitions were started, newsletters circulated, and a body of technical knowledge began to diffuse far more widely than it had before. For the first time since Prohibition, there was a national community of amateur brewers capable of exchanging ideas at scale.

The dissemination of these techniques and recipes contributed to the development of brewing skills in the United States at an unprecedented pace. This was a key starting point for craft brewing as many successful brewers in the coming decades, including some of the craft industry’s pioneers, began their careers as homebrewers. Legal homebrewing allowed these enthusiasts to make the first steps towards professional brewing outside the major brewers, laying the groundwork for the explosion in independent brewing.

From here two further developments help explain how craft brewers managed to overcome the problem of scale and producer monopoly over the last two decades; the popularity of the IPA and developments in equipment contracting would help lower the capital barriers that once forced so many regional competitors out of the market.

The first is that minimum efficient scale, which was the foundation for massive consolidation, varies by beer type. Lagers, the predominant style produced by the large national brewers, typically take around three times as long to brew as IPAs, the favored style of craft breweries. Craft brewers gravitated toward ales not simply out of taste preference, but because ale production aligned well with small-scale equipment. The difference in brew time is nearly threefold from 28–42 days down to 10–14. A brewery operating a ten-barrel brewhouse can cycle through batches of IPA much faster than comparable volumes of lager, allowing capacity to be used more intensively and giving greater flexibility in terms of experimentation.6 This dramatically lowers the economic burden of small-scale production, and opens the opportunity for a new class of smaller breweries. Because fermentation tanks are the binding capital constraint in brewing, faster turnover directly lowers effective capital costs. In the IPA era, equipment that once would have limited brewery volume to serving a brew-pub could now support a financially viable business with modest regional distribution.

For most of the early craft era, draft beer was the economic backbone of craft brewing. Draft carries unusually high margins because it bypasses the most expensive stages of production: bottling and canning equipment, packaging materials, line labor, and the distribution markup. A brewpub selling beer across its own bar could convert a fermenter of ale into finished product with minimal additional cost, which is part of the reason the 1980s and early 1990s craft landscape was dominated by on-premise breweries rather than packaging plants. Draft allowed small producers to survive without the capital expenditure required to reach store shelves or regional markets.

The second development is the rise of contract brewing and mobile canning, both of which further reduced the capital requirements for market entry and distribution. Brewers like Boston Beer Company built their initial success by leasing tank space from existing regional breweries, using their facilities to benefit from economies of scale before investing in their own infrastructure. Today this practice is even more common. Many regional breweries contract out excess capacity to smaller firms, creating a flexible production ecosystem that stands in stark contrast to the rigid, vertically integrated operations of the mid-20th century. 7

Packaging innovation further accelerated this shift. Historically, canning was one of the most capital-intensive components of beer production. A dedicated canning line could cost hundreds of thousands of dollars to construct and thousands more to maintain, an insurmountable barrier for most start-ups. In the early 2010s, mobile canning companies emerged as a solution, bringing industrial canning equipment directly to breweries. These services allow small producers to package beer for distribution without purchasing their own machinery.8 They also allow breweries to experiment with new products that might not justify investment in a full production line.

Canning removed one of the most significant structural barriers to growth, allowing the high-margin draft model to serve as a springboard rather than a ceiling. The result was again the transformation of craft brewing from a largely local, on-premise phenomenon into a national market with thousands of producers competing on shelves that had once been the exclusive domain of the big three. Both were major economic shifts, transforming fixed costs into variable costs for new brewers, enabling easier exit and entry.

Further, from 2000 onward, the antitrust landscape also saw a shift. The wave of global brewing mergers, especially the creation of SABMiller and the later rise of Anheuser-Busch InBev, forced U.S. regulators to reconsider whether efficiency claims could still justify extraordinary levels of concentration. The DOJ’s 2008 review of the InBev–Anheuser-Busch merger marked a turning point. Although the merger was ultimately approved, the remedy required divesting the domestic rights to Labatt’s U.S. business due to excessive concentration in the Buffalo, Rochester and Syracuse metropolitan area, signalling a growing sensitivity to the risk of coordinated effects among remaining large firms. 9

That trend intensified with the proposed 2016 acquisition of SABMiller by AB InBev, one of the largest beverage mergers in history. Here, the DOJ’s consent decree went further: AB InBev was required to divest all SABMiller’s U.S. assets (including the MillerCoors joint venture) to Molson Coors, holding the market US share constant, as well as unwind a portfolio of several other international brands. Regulators imposed additional conduct restrictions on AB InBev’s relationships with independent distributors, requiring a 10% cap on national distribution ownership and locking in existing wholesaler contracts.10 For the first time, antitrust authorities explicitly recognized the competitive importance of distribution access in beer markets, not just production capacity, prohibiting AB InBev from using incentive programs that would discourage distributors from carrying rival craft brands. This represented a major conceptual shift away from the narrow price-centric view and toward a model closer to mid-century structuralism, updated for the realities of a vertically complex beer market.

Since the craft beer boom, the core antitrust problem in beer has been less about the number of breweries than about control over access. Mid-century enforcement focused on producer mergers because that was where power accumulated. By the 2000s, the landscape looked different. Thousands of small craft brewers coexisted with the two global giants, and yet craft access to shelves and taps increasingly depends on a shrinking number of distributors bound by franchise laws and long-term contracts. Regulators were slow to recognize that bottleneck power in distribution could be as consequential as consolidation in production, but the 2016 consent decree and 2018 final judgement marked a shift: antitrust policy began to treat distribution exclusivity and incentive structures as mechanisms capable of distorting competition.11

In this sense, the modern antitrust approach acknowledges what had been true for decades but only implicitly addressed: beer markets are shaped not simply by how many firms exist at each respective tier, but by the contractual and structural linkages between those tiers. Whether in the national mergers of the twentieth century, the global consolidations of the twenty-first, or the exclusive-dealing agreements that saturate contemporary distribution, the central antitrust question in beer has always been the same. When access collapses into a single channel, whether through merger, regulation, or contract, the market begins to look less like a competitive field and more like a stadium concession stand.

Together these developments made it possible for small breweries to thrive even as national demand held steady. Consumer preferences shifted alongside these developments toward higher-priced, stronger beers, further supporting margins that small producers needed to operate. The resulting market is extraordinarily diverse. Yet, as the example of stadium pricing reminds us, diversity of choice at the producer level does not guarantee competitive outcomes for consumers. Distribution remains a key variable.

State-Level Structure and Distributor Consolidation

The national picture of producer growth does not capture the key role that state-level regulation plays through the three-tier system. In a state like Vermont, where breweries, distributors, and retailers must remain legally distinct entities, there has been a clear trend toward consolidation in distribution and wholesale markets while brewery density hits all-time highs.12 Distributor consolidation creates a worrying bottleneck. Firms that control distribution can decide which products are widely available and which remain confined to taprooms. This can influence pricing, product visibility, and even the survival of small breweries while remaining largely invisible to the consumer.

Even as the number of breweries increases, wholesale and transportation markets have grown more consolidated regionally. This is because states often require producers to sell through a licensed state distributor, which makes distributors a legally required intermediary, with some states barring self-distribution entirely. When the number of distributors shrinks, their bargaining power increases. A brewery may face dozens of local competitors, but with only a handful of distributors willing to carry its products, the competition is over distribution contracts. In this sense, wider distribution resembles our basic stadium example: an environment in which a single channel largely determines what choices reach consumers.

In most franchise-law states, once a brewery signs with a distributor, that distributor effectively gains exclusive rights to the brand within its region. Termination typically requires demonstrating “good cause,” a standard that is higher than in normal commercial contracting and often requires litigation or binding arbitration, and in many cases grants wholesalers an opportunity to cure the deficiencies alleged in a termination notice.13 The effect is to invert bargaining power: the brewery becomes locked into a long-term relationship with a much larger wholesaler, whose incentives may or may not always align with promoting its products.

These constraints fall especially heavily on small and mid-sized craft breweries. Unlike national brands, which guarantee distributors high-volume, high-stability sales, craft breweries depend on frequent seasonal releases, rotating taps, and direct relationships with retailers. When the distributor tier consolidates, these smaller breweries often lose visibility and bargaining leverage. Even breweries with strong local demand can find themselves unable to maintain shelf space or secure tap lines when wholesaler portfolios become saturated.

Vermont provides a recent, concrete example of how fragile distribution access can be. VT Beer Shepherd, one of the major craft-focused distributors in the state, ceased operation in 2025.14 According to reporting, many of the larger breweries in their portfolio were quickly absorbed by the three remaining major distributors, again deepening concerns about concentration, but several smaller brewers were caught off guard by the closure and had trouble finding someone to pick up distribution, losing out sales. Beer Shepherd was further one of the only distributors that offered short-term, festival-style distribution arrangements for out-of-state breweries. Other distributors in the region tend to require two- to three-year contracts, a commitment that many smaller festival-bound producers cannot make, especially from outside the region of normal distribution. With no one to fill that niche, several brewers that would normally appear at major events and trickle down to shelves intermittently have decided to forgo Vermont distribution altogether.

Beer Shepherd’s closure mattered not because it was large, but because it occupied a niche that no other distributor in the state had any incentive to fill. Its portfolio favored small producers, and it offered flexible, short-duration contracts uncommon in a franchise-law environment. In its absence, breweries with modest volumes or experimental products are more likely to be overlooked by the major wholesalers whose portfolios prioritize predictable, high-volume brands. The loss of even one such distributor can therefore reshape the competitive landscape in such a way that resembles the homogenization that occurred under brewery consolidation.

The disappearance of an independent distributor of this type narrows the pathways available to craft breweries seeking local distribution. It highlights a pattern seen nationally, where producer diversity masks growing concentration further down the supply chain. The result is a market structure where breweries face intense competition among an increasingly constrained distribution system. Some breweries, like Treehouse in Massachusetts, have even decided to opt out of distribution entirely and only sell on-premises from their own retail locations.

While states are the primary focus of brewing legislation, county and municipal laws can hold a significant bearing on day-to-day operations. There are still counties and towns that hold a maximum limit of licenses issued to bars and taprooms, others have policy instruments to levy additional taxes or limit pricing, and some outright prohibit the sale of alcoholic beverages within their jurisdictional limits. Though outright prohibition is rare, these considerations pose serious regulations on the opening and operation of brewing, service, and retail establishments. These represent the additional local incentives for business operation and largely reflect constraints on the point of service.

An International Perspective: The UK Tied House System

The legal-institutional component in the United States’ unusual success in fostering craft brewing becomes clearer when contrasted with the United Kingdom’s tied house system. The problem of low-quality or monotonous beer in the UK, at least through the 20th century, was the legacy of anti-competitive practices in distribution among pubs and the “big six” brewers who by 1976 controlled 83% of the market.15 The tied house system, which linked pubs to major breweries by direct ownership or exclusive supply contracts, created substantial barriers to market entry. Whereas the United States legally separated brewing and retail after the repeal of Prohibition, the British model embedded the retail level within a vertically integrated production and distribution structure.

The tied-house system emerged in the late nineteenth century as breweries purchased pubs to secure stable retail outlets in an increasingly competitive market. By controlling the pub estate, breweries could guarantee distribution for their products while excluding rivals. Over time, the system hardened into a structural barrier: access to consumers was determined not by product quality or innovation but by ownership and long-term supply contracts.

The Campaign for Real Ale (CAMRA) is a UK-based consumer organization founded in 1971 to protect and promote traditional British cask-conditioned beer, what it termed “real ale.” At the time, Britain’s beer market was rapidly consolidating, and major breweries were abandoning cask ale in favor of more American style keg beer, which was filtered, pasteurized, and force-carbonated for longer shelf life and easier handling. CAMRA emerged as a grassroots response against this industrial shift, arguing that cask ale represented both superior quality and an important British cultural tradition.

However, CAMRA’s influence was largely cultural and consumer-facing, not structural. It could shape taste, advocate for traditional production, and elevate independent brewers in festivals and independent pubs, but it had no authority over the laws regulating the tied-house system, or the ownership and supply contracts through which breweries and later pub companies controlled which beers were sold in pubs. CAMRA could build demand for independent or cask ale, but it could not force pub-brewery owners and managers to respond against their own interest.

In this environment, pubs were ultimately limited in what beer they could serve. Small breweries wishing to enter the market had limited access to consumers in the high margin draft market unless they owned and managed their own tied houses, an option that required significant capital and real estate investment. The Beer Orders of 1989 attempted to break up this system by requiring large breweries to divest portions of their pub estates and allow tenants to offer at least one guest tap for outside producers.16 Yet this reform led to the rise of large pub companies, or pubcos, like Greene King and Wetherspoons which purchased the divested pub properties and then negotiated their own supply contracts.17 In effect, the structure of the market shifted, with the orders repealed in 2003 after effectively breaking the “big six” oligopoly, but the underlying barriers simply changed hands.

The UK today boasts many excellent craft breweries but finding them is still often difficult. Shelf space, tap lists, and distribution channels are controlled not by independent retailers but by corporate groupings whose incentives still favor large suppliers. The consumer’s experience is therefore shaped less by the total number of breweries operating in the country and more by the structure of access at not just distribution but point of service. The contrast reinforces the importance of competition across the American three-tier system in promoting a diverse beer culture.

This makes the UK a useful foil for the American experience. In the United States, the post-Prohibition separation of production, distribution, and retail, however unevenly enforced, prevented any one firm from establishing full vertical market consolidation. The UK moved in the opposite direction and broke up the vertically integrated monopolies rather late in the game. By dismantling brewery-owned tied houses and allowing pub companies to acquire massive estates of pubs, it replaced one form of vertical integration with a new horizontal one, constructing a system in which the retail tier remained the primary barrier to entry under different ownership. As a result, craft beer in the UK grew more slowly, with fewer breweries reaching national or international distribution. The contrast highlights the importance of retail access: even with a vibrant brewing culture, innovation stalls when the last link in the chain remains controlled by a small number of gatekeepers.

Stadium Pricing and Market Capture

Having surveyed some national, international, and state-level features of the beer market, we can return to stadium pricing with a clearer understanding of how the issue emerges and why it resonates. The stadium offers a highly visible, condensed version of the monopoly logic that appears as an undercurrent throughout the history of American beer. Inside a stadium, access is controlled by a single concessionaire often operating under an exclusive venue contract. Consumers have few, if any, alternatives. Producers gain access only by negotiating with that concessionaire. The system is closed, the flow of goods is controlled through a single firm, and the prices charged are as much a function of restricted access as they are of production costs.

This logic applies broadly across the industry. At the national level, scale, control over distribution networks and advertising budgets drove consolidation. At the state level, mandatory three-tier systems create legally enforced bottlenecks at the distributor and wholesale tier. In the UK, tied house systems recreated similar barriers by linking pubs to their suppliers. In each case, the critical variable is not the total number of breweries in existence, but who controls the pathway between brewing and consumption. This is where the institutional perspective becomes important.

Stadiums illustrate this principle sharply because the barriers are immediately visible to the public. A fan who wants a beer at a game cannot choose to shop elsewhere, they are physically prevented from doing so. But similar constraints operate in more subtle forms throughout beer markets, shaping what ends up on store shelves and tap lines. What stadium pricing shows is that beer markets do not naturally produce competitive prices or diversity of offerings. Instead, outcomes depend on the underlying structure of access. Lina Khan’s comments point to this broader truth: that unconscionable prices arise not from consumer preferences for ticket-beer price pairing but from the absence of meaningful choice.

So, what does this mean for the debate over a proposed price cap? Well, let’s look at the corporate structure of Yankee Global Enterprises. The stadium is directly operated by the company, but concessions are contracted out to Legends Hospitality, a joint venture that is partially owned and independently operated from YGE. Even before we get into any of the details of beverage procurement, this already complicates the basic model of a price cap. What looks from the outside like a single seller charging monopolistic prices is, internally, a multi-layered organizational structure with overlapping incentives, revenue-sharing arrangements, and contractual obligations that do not map neatly onto the standard model of a dominant firm maximizing its profit.

In practice, concessions being outsourced can be priced under different incentives. Stadium operators negotiate long-term contracts with vendors, and those contracts often include revenue-sharing provisions, exclusivity clauses, minimum-revenue guarantees, and performance metrics that shift multi-product pricing decisions away from what a firm might choose under unified ownership.18 Legends, for example, operates concessions at several large venues, not just Yankee Stadium, and its financial incentives are connected as much to its broader portfolio as to any one site. Yankee Global Enterprises, by contrast, captures value through ticketing, broadcast rights, sponsorships, and premium seating rather than just marginal concessions sales.19

The relevant point is straightforward: when two partially aligned firms share control over multiple overlapping market, in this case, the sale of beer and tickets, the resulting price changes will reflect the structure of the underlying contracts. In these vertically separated but contractually linked arrangements, each firm optimizes given the other’s terms, creating pricing outcomes that cannot always be modelled as simple price-setting monopoly behavior.

This matters because a tidy single-firm optimization story loses explanatory power when we consider the equilibrium effects of a price cap. Stadium prices are not set the way a textbook monopoly would set them, even if the outcome looks very similar. The concessionaire bears the costs of labor, procurement, and inventory management. The stadium controls the physical space, the brand, and the captive audience. Each party wants to maximize its own return, but the revenue-sharing agreement determines how much of each additional dollar goes where. In some contracts, the stadium receives a percentage of gross sales, which means both parties prefer higher prices. In others, the concessionaire pays a fixed fee for the right to operate and then keeps the marginal revenue, which diminishes the venue incentives to support high prices significantly. Under exclusivity arrangements, a concessionaire may pay substantial upfront fees for the right to be the sole provider of beer, food, or merchandise, and those fees must be recouped through sales. The pricing structure that emerges is therefore a function of contract design as much as market power, and the pass-through effects of a price-ceiling must be transmitted through these channels, subject to frictions as margins are adjusted and contracts are renegotiated.

This is why a price cap is both more complicated and more revealing than it appears. A municipal price ceiling on beer inside a stadium would not simply reduce the profits of a single firm or proportionally raise ticket prices. It would interfere with a set of contracts that allocate risk, reward, and bargaining power across two or more corporate entities. If beer prices fall, is it Legends, YGE, or ticket buying consumers that absorb the loss? Does the cost get passed through to vendors in higher internal fees? Does the contract automatically adjust, or does the concessionaire seek renegotiation? Policies aimed at consumer-facing prices in vertically or contractually fragmented markets often work their way backward through the chain, altering incentives in ways that do not necessarily lead to the intended or even expected outcome from a basic theory perspective.

There is value to drawing on basic theory to understand that there is some deadweight loss, but the actual distribution and magnitude is going to meaningfully be a function of market structure and institutional frictions, which seems somewhat lost in the price cap debate. Constraints and frictions, cutting marginal returns or shifting price-setting power to bidders, reshapes firm incentives and fundamentally alters payoff structures. The directional impact on pricing may resemble competitive outcomes, but the consumer welfare implications can differ markedly due to changes in allocative efficiency, targeting, or surplus extraction.

The difficult and underwhelming answer is that a complete analysis of the effects of a price cap on the cost of a stadium beer has multiple frictions it must account for if we want to reliably determine the equilibrium outcome, and magnitude of the welfare effects for stadium goers.

In Conclusion

The issue of stadium beer pricing may seem, at first glance, outside the scope of a larger economic history of American beer. Yet it is deeply connected to the themes explored throughout this project. Stadiums provide a visible example of monopolistic pricing, contract frictions, and supply chain constraints, demonstrating how structure, rather than consumer preference, can determine market outcomes. This logic repeats across brewing history, from mid-century consolidation to contemporary distribution bottlenecks. By examining how access is controlled, nationally, internationally, and at the state, municipal, and venue levels, we can better understand the forces that shape the contemporary American beer landscape.

If we have learned anything it’s that greater competition across brewers, distributors, and retailers makes for better beer.

Hoffman, Liz. “Lina Khan’s Populist Plan for New York: Cheaper Hot Dogs (and Other Things).” Semafor, 2025. https://www.semafor.com/article/11/12/2025/lina-khans-populist-plan-for-new-york-cheaper-hot-dogs-and-other-things

Tremblay, Victor J., and Carol Horton Tremblay. The U.S. Brewing Industry: Data and Economic Analysis, 2005.

FTC. “The Brewing Industry” Staff Reports of the Bureau of Economics. 1978. https://www.ftc.gov/sites/default/files/documents/reports/brewing-industry/197812brewingindustry.pdf

Elzinga, Kenneth. “Beer.” In Handbook of Industrial Organization, 1989.

US DOJ. “U.S. v. Pabst Brewing Company, et al.” 1971. https://www.justice.gov/atr/case/us-v-pabst-brewing-company-et-al

Briggs, Dennis E., Chris A. Boulton, Peter A. Brookes, and Roger Stevens, Brewing: Science and Practice. Cambridge: Woodhead Publishing, 2004

Brewers Association Seminar. “The Ins and Outs of Contract Brewing”. 2025. https://www.brewersassociation.org/seminars/the-ins-and-outs-of-contract-brewing/

Brewbound. “Mobile Canning vs In-house Canning Lines: A Classic Example of an Insource versus Outsource Decision”. 2023. https://www.brewbound.com/sponsored/mobile-canning-vs-in-house-canning-lines-a-classic-example-of-an-insource-versus-outsource-decision/

US DOJ. “Justice Department Requires Divestiture in InBev’s Acquisition of Anheuser-Busch: Divestiture Preserves Competition for Beer in Upstate New York.” 2008. https://www.justice.gov/archive/atr/public/press_releases/2008/239430.htm

Merced, Michael J. de la. “Anheuser-Busch InBev Merger With SABMiller Wins U.S. Antitrust Approval”. New York Times, 2016 https://www.nytimes.com/2016/07/21/business/dealbook/anheuser-busch-miller-merger-wins-us-antitrust-approval.html

US DOJ. “U.S v. Anheuser-Busch InBev SA/NV and SABMiller plc”. 2018. https://www.justice.gov/atr/case/us-v-anheuser-busch-inbev-sanv-and-sabmiller-plc

Vermont Department of Liquor and Lottery. “Laws and Statutes Related To Alcohol and Tobacco”. Vermont DLL, 2024. https://liquorcontrol.vermont.gov/laws/laws

Sorini, Marc E., McDermott Will & Emery LLP. “Beer Franchise Law Summary” Counsel for the Brewers Association, 2014. https://www.brewersassociation.org/wp-content/uploads/2015/06/Beer-Franchise-Law-Summary.pdf

Kendall, Justin. “VT Beer Shepherd Ceases Operations; Baker Distributing Acquires Part of Portfolio, Including Lawson’s” Brewbound, 2025. https://www.brewbound.com/news/vt-beer-shepherd-ceases-operations-baker-distributing-acquires-part-of-portfolio-including-lawsons/

Curtis, Matthew. “Independence versus authenticity” CAMRA, 2024. https://wb.camra.org.uk/2024/11/07/independence-versus-authenticity

UK Statutory Instruments. “The Supply of Beer (Tied Estate) Order 1989.” 1989. https://www.legislation.gov.uk/uksi/1989/2390/contents/made

Cabras, Ignazio, and David Higgins. “Beer, brewing, and business history.” Business History, 2016, 58(5), 609–624.

Motsinger, S. E., Turner, E. T., & Evans, J. D. “A Comparison of Food and Beverage Concession Operations in Three Different Types of North Carolina Sport Venues” Sport Marketing Quarterly, 6(4), 43-52. 1997.

Howard, Dennis Ramsay, and John L. Crompton. Financing Sport: “Chapter 11: Ticket Sales and Operations” Fitness Information Technology, 2004.